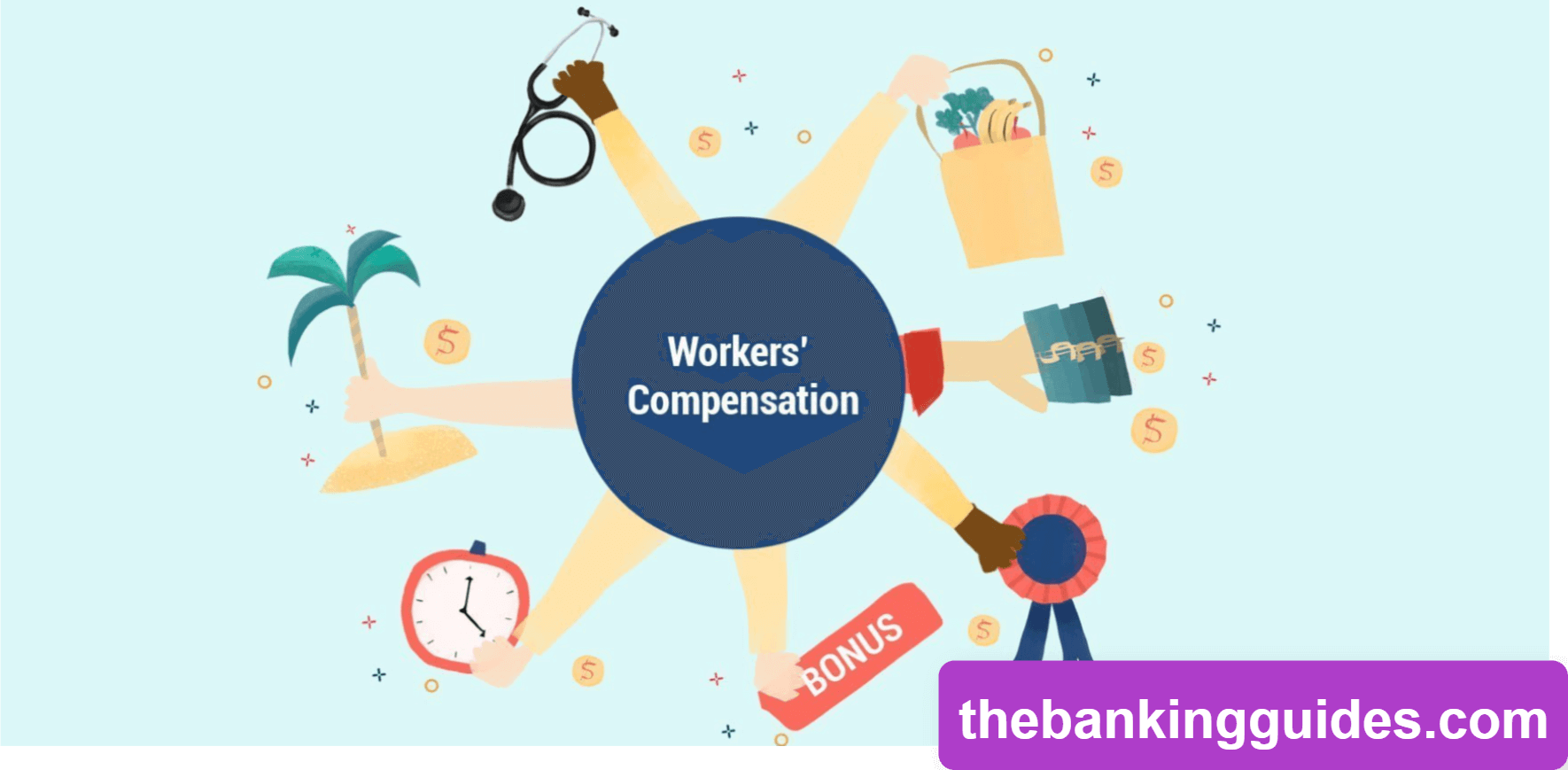

Workmen compensation, commonly known as “workmen’s comp,” stands as a government-mandated initiative designed to offer assistance to workmen facing injury or illness due to their job responsibilities. Functioning as a form of disability insurance, this program extends cash benefits, healthcare benefits, or a combination of both to workmen directly impacted by job-related injuries or illnesses.

In the United States, the administration of workmen compensation is primarily the responsibility of individual states, resulting in significant variations in required benefits from one state to another.

Notably, Texas stands as the sole state that doesn’t mandate employers to maintain workmen compensation insurance.

Navigating Workmen Compensation: A Comprehensive Guide

Workmen compensation benefits may encompass partial wage replacement for the duration when the workman is unable to work. Additionally, these benefits might include reimbursement for healthcare services and occupational therapy.

Typically, workmen compensation programs are funded by private insurers through premiums paid by individual employers. In each state, a Workmen’s Compensation Board, functioning as a state agency, oversees the program and intervenes in disputes.

Federal workmen compensation programs extend coverage to federal employees, longshore and harbor workers, and energy employees. Another federal initiative, the Black Lung Program, addresses death and disability benefits for coal miners and their dependents.

Navigating Workmen Compensation Benefits

Workmen compensation requirements exhibit notable disparities across states, with coverage exclusions and varying criteria. In certain states, small businesses, for instance, may be exempt from mandatory coverage. Meanwhile, different industries may face distinct requirements in other states. The National Federation of Independent Business (NFIB) offers a comprehensive summary of each state’s workmen compensation requirements.

Navigating Workmen Salary Replacement

The salary replacement provided to a workman under workmen compensation is generally less than their full salary, with the most generous programs covering approximately two-thirds of the individual’s gross salary.

Workmen compensation benefits typically remain non-taxable at both the state and federal levels, helping offset a significant portion of the lost income. However, recipients with additional income from the Social Security Disability or Supplemental Security Income programs may be subject to taxes.

Navigating Workmen’s Healthcare Cost Reimbursement and Survivor Benefits

The majority of compensation plans provide coverage for medical expenses solely related to injuries directly resulting from employment. For instance, a construction worker could seek compensation for an injury sustained in a fall from scaffolding but not for an injury occurring during the commute to the job site.

In some scenarios, workers may receive the equivalent of sick pay during medical leave. In the unfortunate event of an employee’s death due to a work-related incident, workmen compensation disburses payments to the worker’s dependents.

Understanding the Waiver of the Right to Sue

When workers opt to receive workmen compensation, they effectively relinquish their right to sue their employer for negligence.

This arrangement, known as the compensation bargain, serves to safeguard both workers and employers. Workers, in exchange for guaranteed compensation, forego pursuing further legal recourse, while employers accept a certain level of liability, avoiding the potentially higher costs associated with a negligence lawsuit.

Exploring Special Considerations

A claim for workmen compensation may face challenges and disputes from an employer, prompting involvement from the Workmen Compensation Board to resolve the disagreement.

Disputes often revolve around the question of whether the employer is genuinely liable for an injury or illness.

The realm of workmen compensation payments is not immune to the risk of insurance fraud. Instances may arise where an employee falsely reports an injury as job-related, exaggerates the severity of an injury, or even fabricates an injury altogether.

In fact, the National Insurance Crime Board highlights the existence of “organized criminal conspiracies of crooked physicians, attorneys, and patients” engaging in fraudulent activities by submitting false claims for workmen compensation and other benefits to medical insurance companies.

Deciphering the Independent Contractor Exception

In most states, eligibility for workmen compensation is limited to regular employees, excluding independent contractors. This distinction emerged as a key point of contention during the debate over a California ballot measure aiming to extend employee benefits to drivers for ride-sharing apps such as Uber and Lyft.

The debate surrounding workmen compensation and other benefits for contract workers, akin to the gig economy, remains a persistent issue. As of 2020, approximately 17 million Americans were engaged in full-time contract work, with an additional 34 million working part-time or intermittently as contractors (Source: Statista, “Number of People Working Independently in the U.S. from 2017 to 2021, by Frequency”).

Navigating the Types of Workmen Compensation

In the United States, the regulation of workmen compensation rules is delegated to individual states. While the U.S. Department of Labor hosts an Office of Workers’ Compensation Programs, its jurisdiction extends solely to federal employees, longshoremen and harbor workers, energy employees, and coal miners.

The absence of federal standards for workers’ compensation has resulted in a notable disparity in policies for similar injuries across different states. Identical injuries can lead to significantly varied compensation outcomes based on the worker’s state of residence. A paper by the Occupational Safety and Health Administration (OSHA) straightforwardly labels the workers’ compensation system as “broken,” estimating that 50% of the costs associated with workplace injury and illness are shouldered by the affected individuals. Furthermore, low-wage and immigrant workers often refrain from applying for benefits.

Workers’ Compensation Coverage A vs. Coverage B Unveiled: Key Insights

There exist two forms of workmen compensation coverage: Coverage A and Coverage B.

Coverage A encompasses all the benefits mandated by the state that an injured or ill employee is entitled to receive from the employer’s insurance. It includes salary replacement payments, medical care, rehabilitation, and death benefits as needed. These benefits are present in all states except Texas, but they vary widely, and certain states exclude specific employees from eligibility.

On the other hand, Coverage B provides benefits beyond the minimums required by Coverage A. These benefits are typically disbursed only if the employee succeeds in a lawsuit alleging negligence or other misconduct by the employer.

Workers who accept workers’ compensation generally waive the right to sue their employers, entering into a no-fault contract. However, in several states, legislation and court decisions have reinstated the employees’ right to sue under strictly defined circumstances. As a result, an employer may choose to procure a policy that combines both Coverage A and Coverage B.

Understanding the Responsibility for Workmen Compensation Insurance Premiums

The responsibility for workers’ compensation insurance premiums lies with the employer. Unlike payroll deductions for Social Security benefits, there is no direct deduction from employees’ pay. By law, the employer is obligated to cover the costs of workers’ compensation benefits as outlined by individual state laws.

Deciphering the Expenses Involved in Workmen Compensation

The cost of workers’ compensation insurance is subject to variation across states, along with the mandated benefits. Rates also differ based on whether employees engaged in low-risk or high-risk occupations are covered.

The fees for this insurance are calculated based on the company’s payroll figures. Illustratively:

- In California, workers’ comp averages 40 cents for every $100 in payroll for low-risk workers and $33.57 for high-risk jobs.

- In Florida, the average is 26 cents per $100 for low-risk jobs and $19.40 for high-risk jobs.

- In New York, the average is 7 cents per $100 for low-risk jobs and $29.93 per $100 for high-risk jobs.

Deciphering the Steps to Apply for Workers’ Compensation

The procedures for applying for workers’ compensation differ from state to state. Generally, a worker experiencing a job-related injury or illness should:

- Document the injury or illness comprehensively, including details, photos, and the names of witnesses when available.

- Report the injury or illness to the employer, who is responsible for filing the claim with the insurer.

- Follow up with the employer’s insurance company to verify that the claim has been filed.

In the event of a claim denial, the option to appeal the decision is available through the state’s Workers’ Compensation Board.

Understanding Exemptions from Workmen Compensation

In general, workmen compensation eligibility is typically limited to salaried employees, excluding contractors and freelancers. However, each state establishes its own set of rules and exemptions. For instance:

- Arkansas specifically excludes farm laborers and real estate agents from eligibility.

- Idaho excludes domestic workers.

- Louisiana excludes musicians and crop-dusting airplane crew members.

Conclusion

With the exception of Texas, every state mandates employers to provide workers’ compensation coverage to certain employees. The rules are state-specific, resulting in numerous exceptions and exemptions. Contractors and freelancers are commonly excluded, and many states limit coverage for specific professions.

Most states offer online resources to help individuals ascertain their coverage under workers’ compensation insurance. For instance, Florida’s Division of Workers’ Compensation provides program details, links to required forms, and a database to check if an employer has coverage.